How Resilient Were Swiss Agri-Food Importing Firms to COVID-19?

Source:123RF9

The agricultural sector as an aggregate proved resilient to the COVID-19 shock. But how did it impact agribusiness firms within the sector? Using the Swiss case, we provide the first set of evidence on how agri-food importing firms survived the pandemic economically.

Early evidence on the trade effects of COVID-19 were done at country levels using aggregate data. In the aggregate, countries may have proved resilient to the pandemic, but we know nothing about how individual agribusiness firms coped with the shock. Also, given the short-lived nature of the pandemic, the use of aggregate data at lower frequency masks many of the underlying heterogeneity.

Impact of the pandemic on agribusinesses

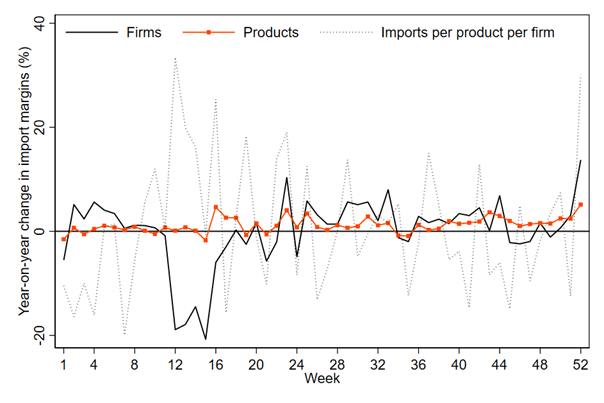

We address these shortcomings and provide the first firm-level evidence of the pandemic on the agri-food sector using daily import data for Switzerland. First, we decompose total imports into three margins: (i) the number of importing firms, (ii) the number of products they import and (iii) the average import value per product per firm (Figure 1). We then study the relationship between the different trade margins and the number of COVID-related deaths per day. We also control for the stringency of the policy response to the shock.

The pandemic reduced Swiss firm-level imports…

A 10% increase in the daily domestic COVID-19 case counts reduced daily product-level imports by 3%. This translates to an average firm-level import reduction of CHF 2,000 per day and a maximum reduction of CHF 208,000 per day. The trade reduction was driven mostly by a decrease in the number of importing firms (see also Figure 1), and comparatively less by the average import values per firm or the number of products imported. At the sector level, consumer goods (e.g., fruits and vegetables) were affected more by the pandemic with intermediate goods (e.g., cereals, live animals, cocoa and products of the milling industry) relatively more insulated.

… even more so for bigger firms

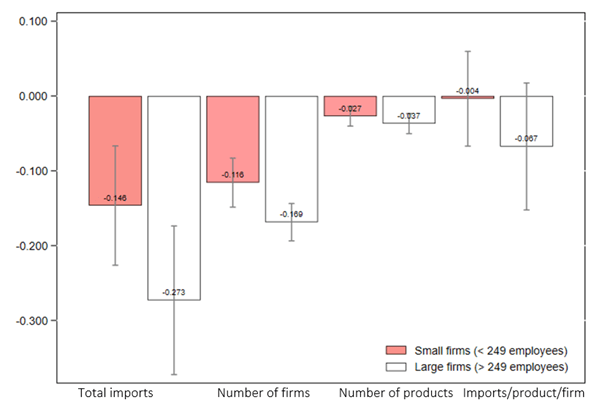

The crisis affected all firms regardless of their size. Yet, larger firms were disproportionately more affected (Figure 2). Different definitions of firm size (inter alia larger employers, larger importers, and firms that import from multiple origins) lead us to the same conclusion. Larger firms are more integrated into global value chains and as a result more prone to global shocks.

Figure 2: COVID-19 and firm-level imports: heterogeneity across firm size.

What mechanisms explain our findings?

Domestically the trade reduction was driven, in part, by lower firm-level productivity induced by the shock. The negative effects we estimate imply that the pandemic’s negative domestic demand effect outweighed its negative domestic supply effect. In response, some firms probably no longer found it profitable to import leading to a reduction in the number of active importing firms. Overall industry productivity also increased which caused even more lower-productivity firms to exit the import market.

We also tested two other mechanisms. First, we checked if there were third-country effects at play. The severity of the shock in other countries and the associated international supply chain disruptions reduced import options of Swiss firms, even if they had the productive capacity to do so. Second, there were changes in Swiss consumer behavior. We find a negative effect of the pandemic on visits to grocery shops and recreational centers, which provides evidence of a decline in consumer demand. We confirm this using information from monthly retailer data.

Conclusions

- We assess how Swiss agricultural imports were affected by the COVID-19 pandemic using daily firm-level import data for 2019 and 2020.

- We observe a reduction in firm-level imports driven mainly by a reduction in the number of importing firms.

- Larger firms were disproportionately more affected by the shock than smaller firms.

- Consumer products were affected more by the pandemic with intermediate goods relatively more insulated.

Bibliographical reference

How Resilient Were Swiss Agri-Food Importing Firms to COVID-19?